China’s gold market in June: wholesale demand stable and gold reserves up

Senior Analyst, China World Gold Council

Key highlights:

Despite June weakness, the LBMA Gold Price AM in USD and the Shanghai Gold Benchmark PM (SHAUPM) in RMB ended the first half of 2023 higher by 5% and 9% respectively – the depreciation of RMB against the dollar over the period contributed to the significant difference

Gold withdrawals from the Shanghai Gold Exchange (SGE) rose by 13t m/m to 125t in June. This puts H1’s wholesale gold demand at 824t, a 16% rise y/y but still below the 10-year average

Mirroring local demand, the Shanghai-London gold price spread rose and then fell in H1, stabilising at US$3.5/oz in June

Despite June inflows, Chinese gold ETFs saw a net outflow of US$74mn (-RMB487mn) during H1, equivalent to a 1t reduction in demand and totalling US$3bn (RMB22bn) or 50t in assets under management (AUM)

The People’s Bank of China (PBoC) announced the eighth consecutive rise in gold reserves in June (+21t). Over the first half of the year China’s gold reserves rose by 103t to 2,113t.

Looking ahead:

Seasonality and the elevated gold price are likely to continue to weigh on local wholesale gold demand in July and, as a consequence, keep the local premium depressed. September brings the traditional jewellery fair and the season for new product launches, which could intensify gold replenishment towards the end of Q3

For a more detailed H2 outlook, please stay tuned for our H1 Gold Demand Trends report, which will be released on 1 August.

The RMB gold price levelled off in June, ending H1 with a sizable gain

Gold prices pulled back last month (Chart 1). Hawkish tones and rate hikes from major central banks, among other factors, weighed on gold. While the SHAUPM fell by just 0.2%, its USD peer witnessed a 3% decline. The RMB gold price’s resilience was mainly due to the local currency’s 2% depreciation against the dollar in June.

Chart 1: The RMB gold price levelled off in June

Note: We compare the LBMA Gold Price AM to SHAUPM because the trading windows used to determine them are closer to each other than those for the LBMA Gold Price PM. For more information about Shanghai Gold Benchmark Prices, please visit Shanghai Gold Exchange.

Source: Bloomberg, Shanghai Gold Exchange, World Gold Council

During H1 both the USD and RMB gold price saw a sizable upsurge. The range-bound dollar and yields, event risk hedging and continued central bank purchases were key contributors. Combined with local currency weakness, the RMB gold price concluded H1 with the highest ever monthly average (Chart 2).

For analysis of H1’s gold price performance and H2 outlook, see our recently published Gold Mid-year Outlook 2023.

Chart 2: The weakening local currency pushed June’s average RMB gold price to a record high*

*Data to 30 June 2023.

Note: We compare the LBMA Gold Price AM to SHAUPM because the trading windows used to determine them are closer to each other than those for the LBMA Gold Price PM. For more information about Shanghai Gold Benchmark Prices, please visit Shanghai Gold Exchange.

**The SHAUPM was listed in April 2016, for data prior to that we use Au9999.

Source: Bloomberg, Shanghai Gold Exchange, World Gold Council

Wholesale demand held steady at the finish of H1

China’s economic revival made a marginal improvement in June. The official manufacturing PMI saw a mild m/m rebound while total social financing increased. But pressures remain. For instance, the y/y growth in vehicle sales decelerated notably in June; meanwhile the CPI and PPI contracted further m/m, indicating weak domestic demand.

Chart 3: Pressures remain for China’s economic revival

Source: Bloomberg, World Gold Council

Gold withdrawals from the SGE amounted to 125t in June, a 13t m/m rebound but a 15t y/y decline (Chart 4). The m/m rebound was likely due to the stabilising local gold price. Nonetheless, demand remained relatively tepid: Q2 is the traditional off season for gold consumption and China’s economic recovery remains uncertain. Our conversations with local gold manufacturers suggest that the 13% y/y surge in the local gold price was the primary reason for the y/y decline in June’s wholesale demand.1

Chart 4: Gold withdrawals were relatively stable in June

*10-year average is based on data between 2013 and 2022.

Source: Shanghai Gold Exchange, World Gold Council

Local wholesale gold demand in H1 was 824t, 16% higher y/y and the strongest in four years (Chart 5). The end of China’s zero-COVID policy was the main contributor to this strength. But figures remain 11% below the 10-year average, as the record local gold price and weakening economic growth momentum dragged down demand.

Chart 5: H1’s wholesale gold demand rebounded but stayed below the long-run average

*10-year average is based on data between 2013 and 2022.

Source: Shanghai Gold Exchange, World Gold Council

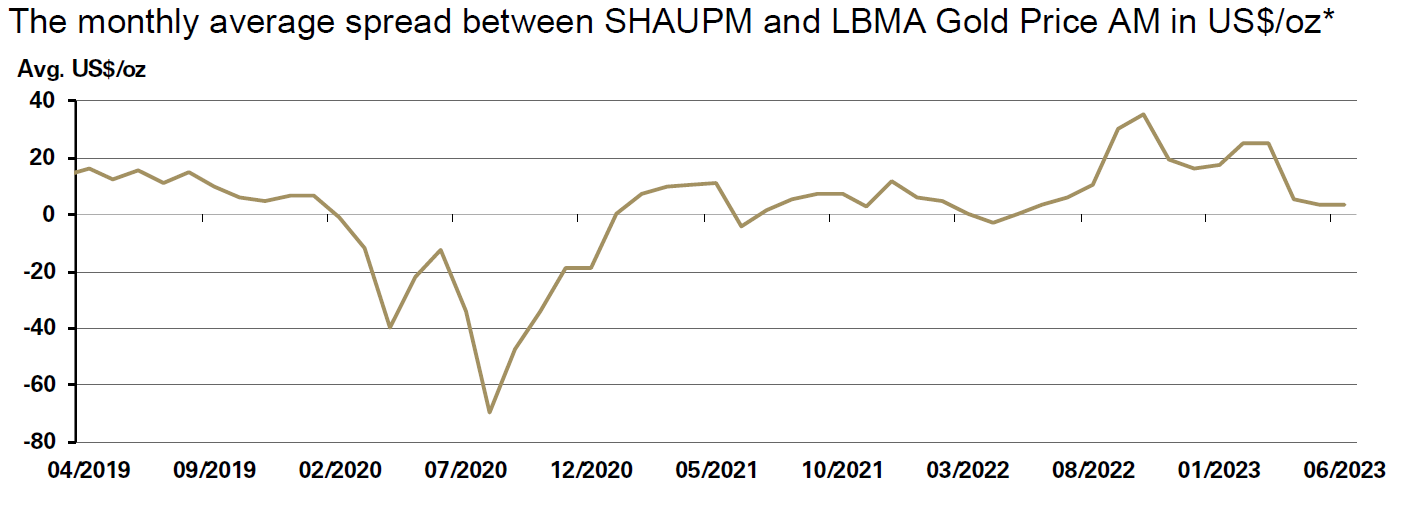

Local premium stabilised, mirroring local demand

The Shanghai-London gold price spread averaged US$3.5/oz in June, virtually unchanged from last month (Chart 4) and a reflection of the stable wholesale gold demand.

And the premium has mirrored changes in H1’s wholesale local gold demand. China’s suspension of the zero-COVID policy in early 2023 caused demand to rebound and optimism to return, driving the spread higher in Q1. But seasonality, a rising local gold price and the weakening economic recovery hindered consumption in Q2, and the premium declined.

Chart 6: The local gold price premium stabilised in June

*Before April 2014 the spread calculation was based on Au9999 and LBMA Gold Price AM; click here for more.

Source: Bloomberg, Shanghai Gold Exchange, World Gold Council

Chinese gold ETFs saw negative demand in H1, despite mild inflows in June

Chinese gold ETFs attracted US$46mn (RMB330mn) in June, the first monthly inflow since March, concluding H1 with an AUM of US$3bn (RMB22bn). Meanwhile, holdings rose by 1t to 50t. As the local gold price stabilised around its record high and the RMB continued to depreciate, investor interest in gold ETFs ticked up.

But overall, H1 saw an outflow of US$74mn (RMB487mn) and a 1t reduction in holdings. Negative fund flows were concentrated in January amid expectations for a strong economic recovery and improved risk appetite. But as economic growth momentum cooled, the RMB depreciated and the local gold price maintained its strength, ETF demand stabilised.

Chart 7: Chinese gold ETFs saw net outflows in H1

Source: ETF providers, Shanghai Gold Exchange, World Gold Council

The PBoC reported its eighth consecutive gold reserve increase in June

The PBoC reported a 21t addition to its gold reserves in June, bringing the total to 2,113t (Chart 8) and accounting for 4% of the country’s foreign exchange reserves. This marks the eighth consecutive increase in China’s gold reserves, amounting to 165t during the period. During the first half of 2023 China’s gold reserves rose by 103t.

Chart 8: China announced another gold reserve rise in June

Source: PBoC, World Gold Council

Imports rebounded in May

China’s gold imports totalled 148t in May, a 24t m/m rise. This amounts to a 121t surge compared with May 2022, at which time key cities were under COVID-related lockdowns.

Chart 9: China’s gold imports rose in May

Source: China Customs, World Gold Council

1Based on SHAUPM’s monthly averages.